AI, Crypto, and Riding Hype Cycle Waves with Brad and Latif

Union Square Ventures co-founder Brad Burnham in conversation with M13 Partner Latif Peracha about lessons learned from decades of venture investing.

Table of contents

The crypto market is different from previous hype cycles. It is both a technology and a financial system.

——Brad Burnham, Union Square Ventures Co-founder

It’s pretty clear that incumbents have massive advantages in data and distribution in AI. But in crypto, they have zero advantages. They’ve tried, but they can’t actually figure it out.

——Latif Peracha, M13 Partner

M13 partner Latif Peracha brought his friend and colleague, Union Square Ventures (USV) co-founder Brad Burnham, to M13’s Future Perfect 2024. Brad shared his insights on the challenges and transformative potential of crypto and AI, as well as on investing in these rapidly evolving technologies.

USV successfully raised its first fund in 2003 by focusing on the application layer of the internet, a contrarian move during the post-dot-com crash period. With this history in mind, Brad acknowledges the importance of timing and of understanding the hype cycles that technologies move through.

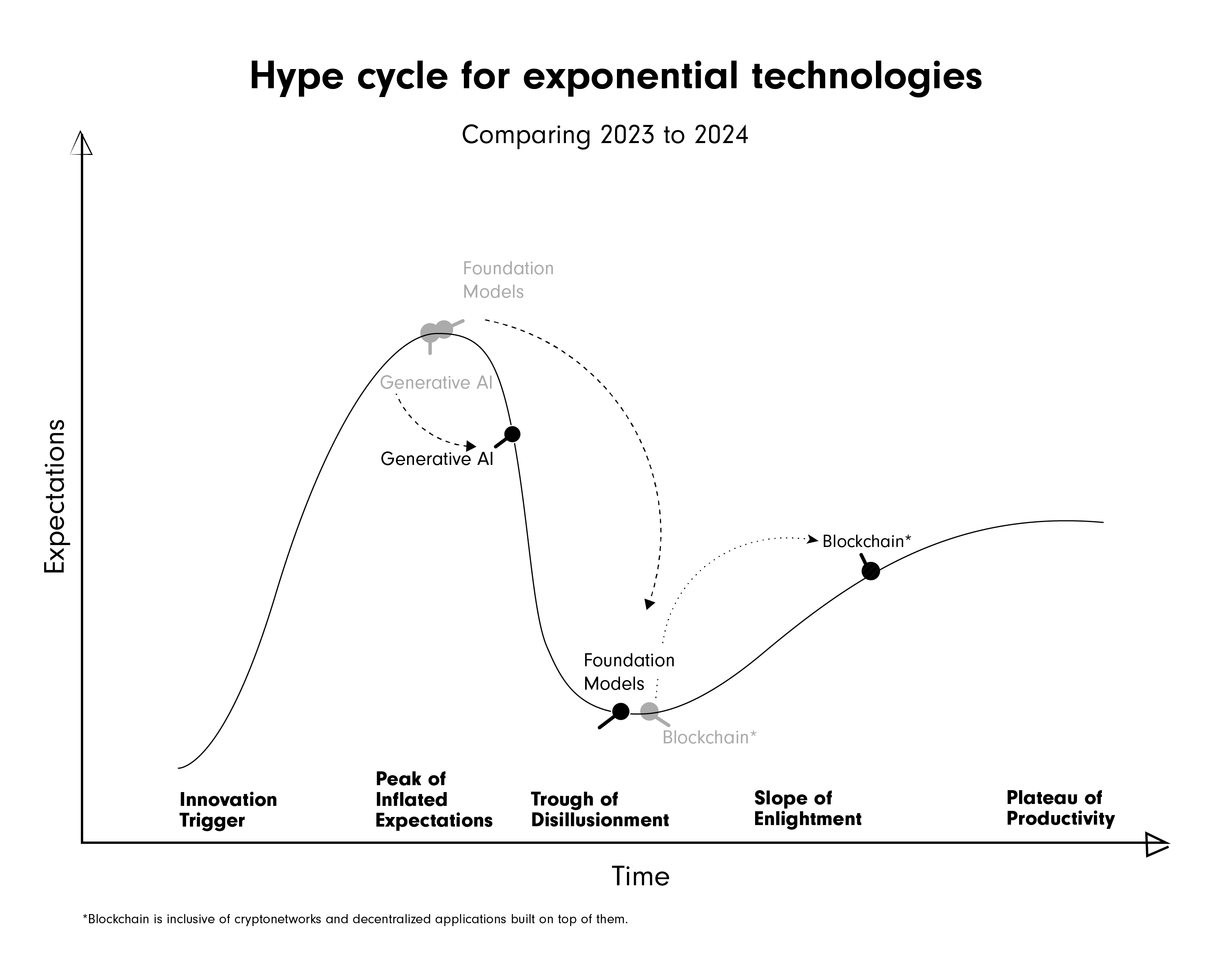

Today, two major hype cycles on investors’ minds are those of AI and crypto. Below, check out some highlights of a sweeping discussion that took our audience from the Industrial Revolution, to the year the Internet broke, to Turkey’s stablecoin adoption (4.3% of its GDP), and even to sound advice from Brad’s mother.

But first, hype cycles: A history

History repeats itself. Carlota Perez, author of Technical Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages, points out that there have been hype cycles around every innovation since the Industrial Revolution. Perez’s book reviews innovations such as steam and railways; steel, electricity, and heavy engineering; oil, automobiles and mass production; and information and telecommunications.

The cycles that have accompanied these major technological shifts created the necessary financial bubbles to drive experimentation, infrastructure development, and ultimately sustained growth. Carlota lays out a few key phases of these cycles:

- Capital mobilization: Bubbles help to rapidly mobilize large amounts of capital needed for infrastructure and innovation.

- Experimentation and innovation: Speculative frenzy encourages a wide range of experiments and innovations, many of which fail (the process of “creative destruction”) but some of which succeed spectacularly.

- Market creation: Bubbles create markets and industries that did not exist before, laying the groundwork for sustained growth during the synergy and maturity phases.

On hype cycle challenges

The unusual crypto case: “We've seen, for the first time, real volatility within a hype cycle,” Brad explains about the crypto market. He compares crypto today with where the internet was in 1995, “the year the internet broke” with the first browser, the first web application, and the first search engines.

“[With crypto], there’s this hint that something really important is going on. A bunch of people have been working on it and thinking about it for a while. But the broader population is unaware of how important it is. You talk to people at cocktail parties and they ask, ‘What’s it good for?’ It’s the same question we used to get in 1995. The underlying architecture does make a difference, and we're about to see real applications.”

The problem with overfunding: Latif describes the difficulty in distinguishing between the financial aspects of crypto projects and the actual technological innovation and development due to their market-driven nature and resulting noise.

Brad acknowledges the unique challenges of investing in publicly traded tokens, including that token offerings result in managing excess funds. "If you happen to do a token offering at a moment in time when there's significant momentum, you could raise a ton of money,” he says. “And it turns out to be really hard to run a company with too much money. You end up over-investing, building big organizations that become unwieldy and you're not actually delivering as fast as you used to.”

In other words: If you've raised so much money that you never have to go back to your investors, the drive to deliver can be diminished. Investing rounds can be a useful framing checkpoint where the decision to reinvest demands disciplined dialogue among investors.

Now for the bright side: Opportunities

An environment of innovation: Technologies need the chance to mature and become useful. Similar to information technology on the internet, crypto and AI are experiencing similar rapid innovation.

"Without that financial bubble, without that enthusiasm, you don't get the experiments that you need in order to put the infrastructure in place to build real systems,” Brad says. "[At USV] we made the argument that we were through the initial crash of the information technology hype cycle, and that we were going to be building now into what Carlota Perez called the deployment period. That’s when a lot of the technologies that were first introduced in the crash actually became important."

Adaptation: "It's our job to figure out how to live with these new problems. It's not the job of the technology or the market to make it easy for us,” says Brad.

Implications: Both investors encouraged looking at the implications of a technology, not just the technology itself. Thinking beyond the infrastructure or core technical pieces brings a huge number of opportunities.

Advice to live and invest by

In closing, Latif asked for advice for investors and founders. Brad offered these two parting insights.

First, “Doing the right thing is a lot harder than doing things right. Doing things right is available to everybody: just keep plugging away. Keep paying attention to your customers, and you can build a business. Doing the right thing is sometimes a matter of luck."

The other piece of advice comes from Brad's mother: "If you marry for money, you pay for it for the rest of your life. Why is that relevant in a venture capital context? Well, if you take the highest offer for your company, if you recruit people using money instead of your mission, you’ll end up paying for it in lots of subtle ways.”

Get in touch

If you are building in crypto and AI and want to talk, please reach out to our investing team: Latif Peracha at latif@m13.co and Mark Grace at mark@m13.co.

The views expressed here are those of the individual M13 personnel quoted and are not the views of M13 Holdings Company, LLC (“M13”) or its affiliates. This content is for general informational purposes only and does not and is not intended to constitute legal, business, investment, tax or other advice. You should consult your own advisers as to those matters and should not act or refrain from acting on the basis of this content. This content is not directed to any investors or potential investors, is not an offer or solicitation and may not be used or relied upon in connection with any offer or solicitation with respect to any current or future M13 investment partnership. Past performance is not indicative of future results. Unless otherwise noted, this content is intended to be current only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in funds managed by M13, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by M13 is available at m13.co/portfolio.

At a glance

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

—Sarah Tomolonius, M13 Partner & Head of Investor Relations

Further reading

.webp)

© 2026 M13. All rights reserved.