3 Myths About M&A and Innovation

M&A is a vital part of the innovation ecosystem, offering a financial incentive for investors and founders to work toward. Here are some common myths we’d like to debunk.

Table of contents

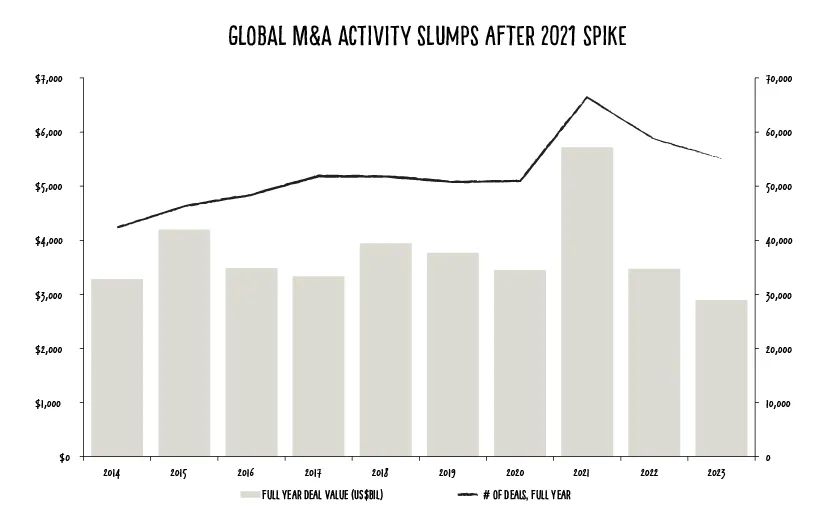

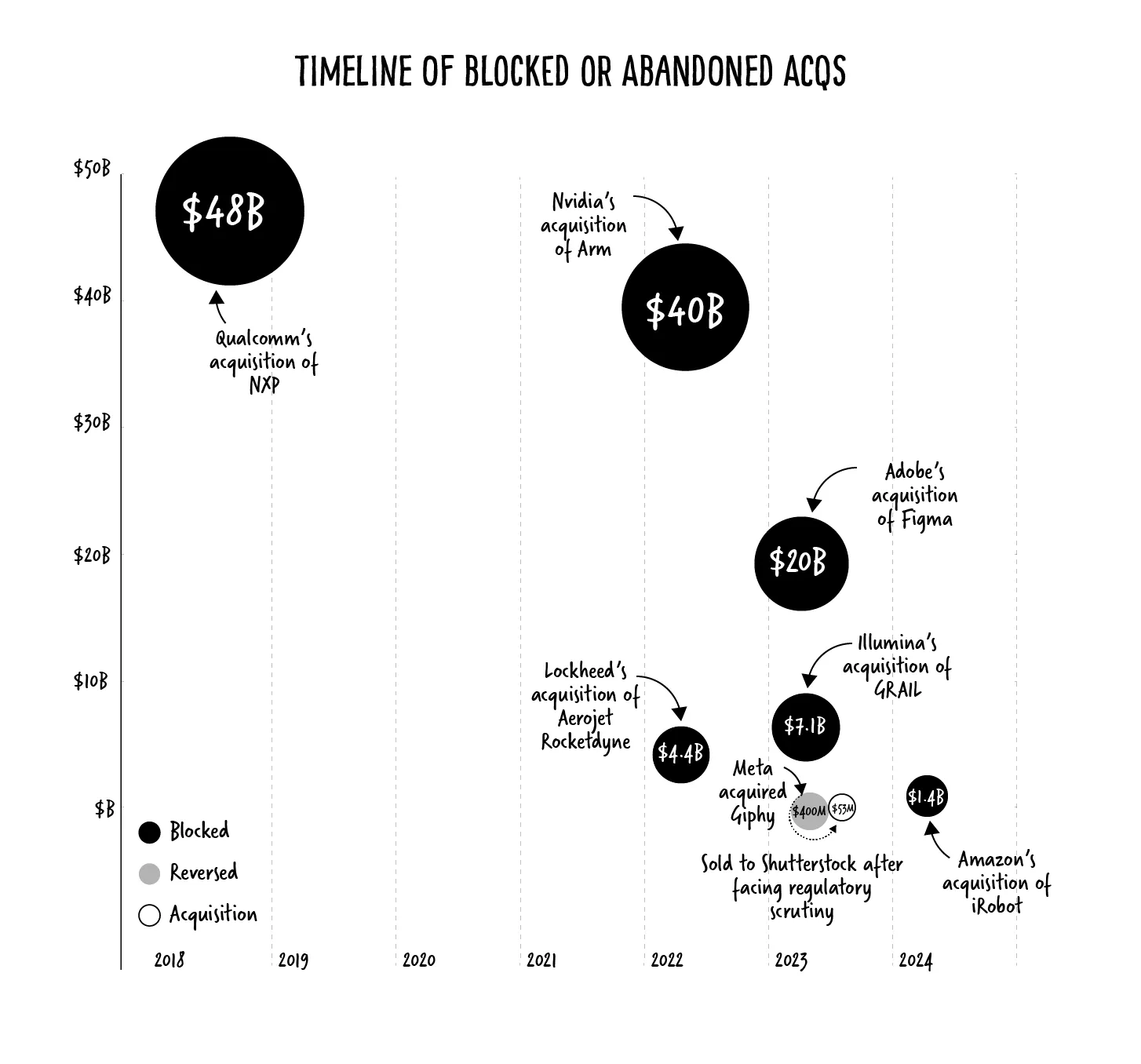

As a venture investor, I find myself thinking a lot lately about the shifting M&A regulatory landscape and its impact on the innovation my industry seeks to support. Last year, worldwide M&A volume fell 17% YoY, reaching a 10-year low. The abandoned $20B Adobe-Figma deal is just one of the latest tech mergers to be squashed by regulators in the name of preserving innovation.

While multiple macroeconomic factors are contributing here, it’s worth paying attention to how regulation has impacted this space.

Notably, as AI has exploded, calls for regulation have also reached a new fever pitch, with FTC Chair Lina Khan recently noting, “There’s no AI exemption from the laws on the books.”

I agree that, to preserve competitive markets, some transactions shouldn’t happen. However, I also believe this should be the exception, rather than the rule. And lately, it seems to be the rule.

Generally, the story is, large mergers reduce the consumer benefits that result from a competitive environment, necessitating regulatory bodies to intervene and block them. But does that argument hold up to scrutiny?

When people in my world—venture investors and the founders they support—hear this argument, we heave a collective sigh. The fact is, M&A deals are a crucial part of supporting innovation and the investment ecosystem needed to foster it. Squashing M&A transactions doesn’t protect innovation; it restricts it.

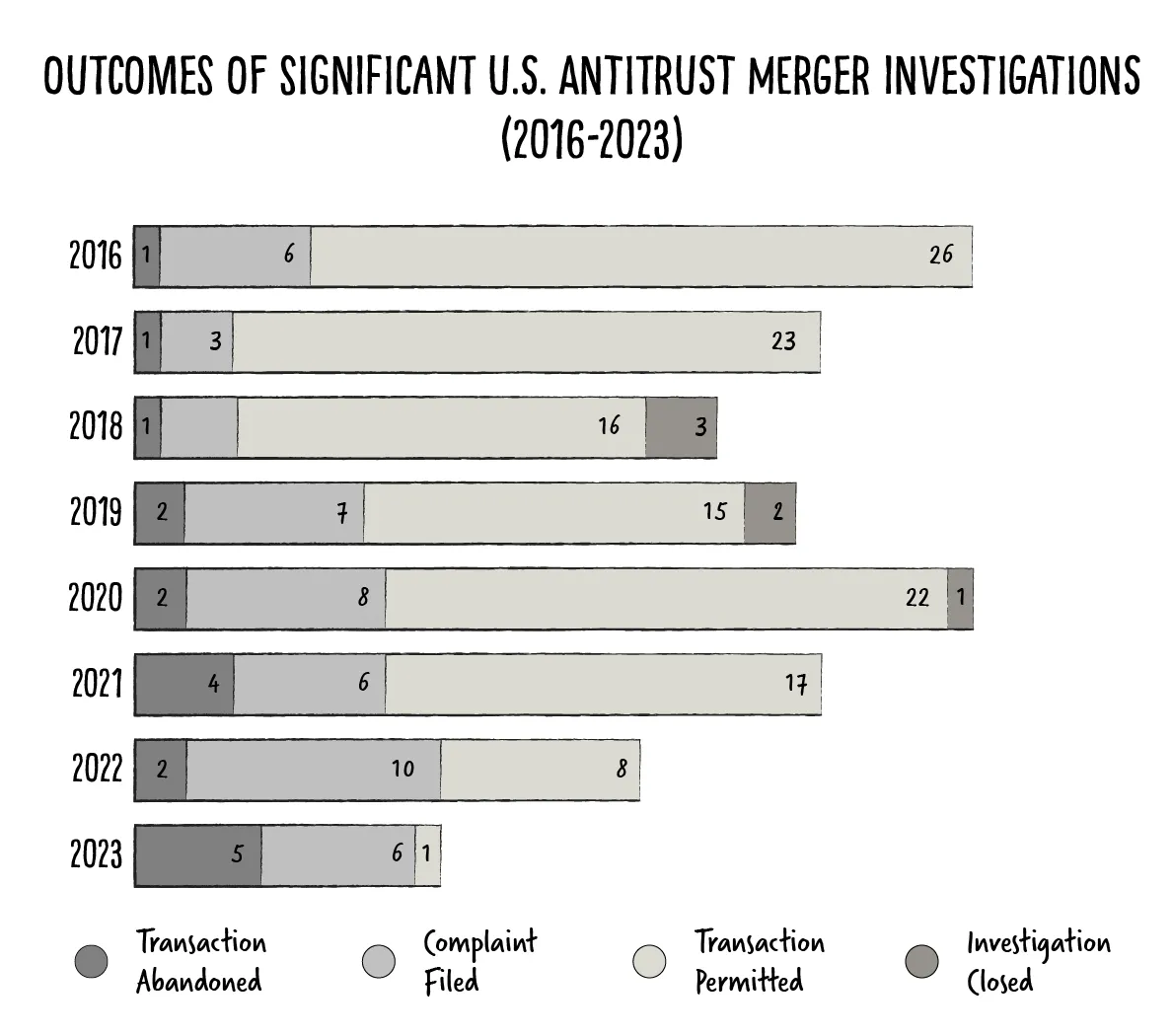

That’s why I get concerned when I see a lower proportion of investigated M&A deals being approved. In 2022, more than half of antitrust investigations led to a complaint or abandoned transaction. By 2023, that ticked up to 92%.

Innovation is at the center of the entire venture capital industry—and venture is uniquely positioned to support it. That in mind, there are a few misconceptions about the relationship between M&A and innovation that I would like to debunk.

Myth #1: Innovation is fed by competition, which is protected by M&A regulation.

Counterpoint: Innovation is fed by investment—and investment is driven partially by returns from M&A.

Creative innovation is hugely driven by the venture investments that support disruptive founders. But while VC firms like M13 are inspired by innovation, it’s important to remember that we are also accountable to our investors. Ultimately, we need to make sound financial decisions.

VCs generally create returns for their investors via two key routes:

- IPO: A portfolio company goes public.

- M&A: A portfolio company gets acquired.

(It is also possible for private companies to become cash flow positive and share dividends to shareholders—but it’s uncommon, and for our purposes, a fairly negligible source of returns.)

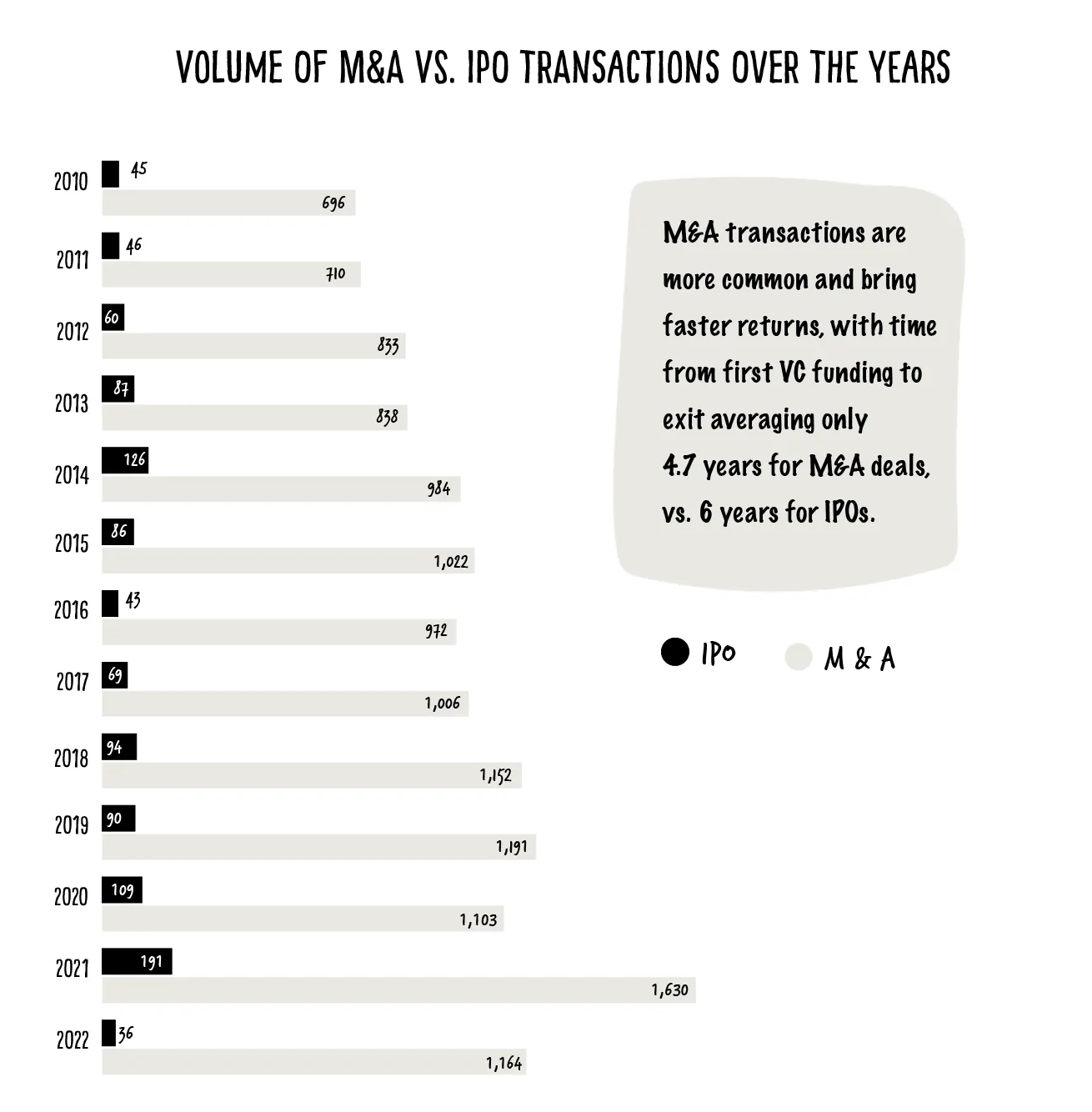

While IPOs generally create better returns, M&A is by far the likelier outcome. In 2022, M&A transactions outpaced IPOs by more than 30x.

While M&A deals generally drive smaller returns, the difference isn’t that vast. One survey found that IPO returns to VC firms averaged 9.7x, vs. M&A returns of 7.4x. M&A transactions also generated returns more quickly, averaging a median 4.7 years between first VC funding and exit, vs. 6 years for companies that IPO.

When regulation takes M&A off the table as an avenue to create returns, VC becomes a less compelling investment category. In turn, Limited Partners (investors in venture funds) become less likely to invest. The end result is that less capital goes to innovators that are feeding the market with new technologies and businesses.

Myth #2: Large mergers discourage founders from innovating in a space.

Counterpoint: M&A not only encourages founders by offering a “finish line” to work toward, but also brings them back to innovating again more regularly.

Venture firms aren’t the only players interested in financial returns from startups; founders and their teams are too. Because it’s difficult for more entrenched firms to truly innovate, more nimble startups are able to monetize on new ideas. As the far more common exit path than going public, M&A creates an invaluable incentive for founders to work toward.

Moreover, founders that successfully exit through M&A often get back the time and freedom to innovate again. For example, after Spencer Rascoff’s Hotwire was acquired by Expedia in 2003, he went on to become co-founder and CEO of Zillow (2011 IPO), in addition to founding myriad other companies (dot.LA, Pacaso, Recon Food, heyLibby, and more). Today, Rascoff continues to feed the innovation ecosystem as an educator, PledgeLA Board member, and General Partner at the VC firm 75 & Sunny.

I believe an ideal outcome of our industry is to allow the world’s greatest innovators to cycle back regularly and innovate a number of times over their careers. M&A deals are one way to release great founders back into the ecosystem so they can build over and over.

“Undue and disproportionate regulatory hurdles discourage entrepreneurs, who should be able to see acquisition as one path to success, and that hurts both consumers and competition—the very things that regulators say they're trying to protect.”

—David Zapolsky, Amazon SVP and General Counsel

Myth #3: Large mergers block consumers’ access to innovative technologies.

Counterpoint: Acquisitions give consumers more access to innovation.

FTC Chair Lina Khan and others often argue that large companies should be innovating on their own, rather than acquiring innovation solutions through M&A deals. I couldn’t disagree more.

Large companies—especially public ones—are terrible at organic innovation. They are limited by short-term performance expectations and restrictive existing technical infrastructure. Moreover, no matter how good a technology is, when it goes to market, over time the uniqueness and the ubiquity of that technology diminishes. This creates an opportunity for smaller, more nimble companies to compete.

In fact, there are many companies that have flourished and provided value to the consumer only because they were acquired by a larger firm that has the ability to continue to fund their operation—such as Facebook’s acquisition of Oculus, or Microsoft’s purchase of LinkedIn. In both cases, tech giants acquired companies that were adjacent to their core business, rather than directly competitive with it. Facebook bet on VR, while Microsoft expanded into business social media.

Because it was acquired by Facebook, Oculus was able to launch its VR product and bring this new technology to millions. Even companies with an existing user base can attain new reach through M&A; Instagram was acquired with fewer than 90 million users, but today boasts more than 2.2 billion.

In short, acquisitions give these smaller companies the resources and reach to offer their innovative solutions to more consumers.

Looking ahead to a better system

I believe the stated goal of regulation is sound: prevent monopolies, enhance competition, and push for new innovation in the market. However, the practices in place today are losing sight of this goal. A few key issues:

- High fees. Antitrust investigations can be costly for the companies being investigated, and increasing scrutiny of M&A transactions can deter companies considering sizable acquisitions.

- Retroactive reversals. Transactions can be overturned even after the deal is finalized—sometimes long after. One extreme case is Axon's $13M acquisition of VieVu in May 2018: the FTC challenged the deal in 2020, sparking a multi-year litigation process.

- Lengthy timelines. It can take months or even years to complete M&A investigations, leaving companies stuck in long holding patterns. Amazon's acquisition of iRobot was abandoned in January 2024 after eighteen months of litigation went unresolved.

Together, these factors discourage companies from entertaining acquisitions and hinder healthy M&A activity in the industry. Many companies are becoming apprehensive about M&A. And many deals that could bring new tech to the market aren’t even being considered, or are being rejected for the wrong reasons.

Knowing the shortcomings of the current system, I think a better system would isolate regulatory assessments to a question of monopolies. Most major acquiring firms should not be able to merge with their major competitors. However, the acquisition of adjacent offerings or smaller extensions to existing products should be allowed, as this drives more distribution, further innovation, and more disruption over time.

Let’s really focus on driving innovation in our world. Let’s give high-risk early investors a chance to establish strong returns and cycle their money back into more innovation. Let’s let the best founders find homes for their companies, so they can move on to build the next major disruptor. Finally, let’s allow the consumer to benefit from allowing disruptive offerings to improve the services and value they receive every day in the market.

The views expressed here are those of the individual M13 personnel quoted and are not the views of M13 Holdings Company, LLC (“M13”) or its affiliates. This content is for general informational purposes only and does not and is not intended to constitute legal, business, investment, tax or other advice. You should consult your own advisers as to those matters and should not act or refrain from acting on the basis of this content. This content is not directed to any investors or potential investors, is not an offer or solicitation and may not be used or relied upon in connection with any offer or solicitation with respect to any current or future M13 investment partnership. Past performance is not indicative of future results. Unless otherwise noted, this content is intended to be current only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in funds managed by M13, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by M13 is available at m13.co/portfolio.

At a glance

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

There are no Cinderella stories. Blockbuster venture successes are always preceded by years of sleepless nights.”

—Sarah Tomolonius, M13 Partner & Head of Investor Relations

Further reading

.webp)

© 2026 M13. All rights reserved.